In light of the regulatory updates announced by Otoritas Jasa Keuangan ("OJK") in June, financial institutions (FIs) in Indonesia are required to strengthen their compliance measures within six months from announcement. This change will bring about strengthened alignment of Indonesia FIs with the international principles governing anti-money laundering programs and prevention of financing for terrorism and weapons. Indonesian financial organisations aiming to achieve compliant digital customer onboarding while maintaining a seamless and secure experience for their customers can consider various best practices and key considerations when selecting the appropriate tools or solutions.

What is the regulatory update about?

In June 2023, Indonesian Financial Services Authority (Otoritas Jasa Keuangan or in short "OJK") announced regulatory updates (announcement in Bahasa) to address money laundering, terrorism financing, and proliferation of mass destruction weapons. The new regulation seeks to now scope in trusts, crowdfunding platforms, and FinTech or Digital Financial Innovation firms as Financial Institutions and subject them to Anti-Money Laundering-Counter Financing of Terrorism (AML-CFT) and Counter Proliferation Financing (CPF) obligations. This regulation will supersede any conflicting article from the previous regulation, POJK Number 12 of 2017, as amended by POJK Number 23 of 2019.

The new regulation also clarifies and enhances existing AML-CFT obligations in areas of risk assessment, proliferation financing, customer due diligence and compliance management. The maximum ceiling of fines on FIs is increased to ensure the effectiveness, proportionality and dissuasiveness of administrative sanctions for AML-CFT and CPF violations.

Financial institutions will have a six-month transition period to comply with the revised regulation.

What does the regulation mean for Financial Institutions in Indonesia?

The new regulation requires financial institutions to implement policies and procedures to prevent money laundering, terrorist financing, and the financing of weapons of mass destruction. This includes conducting customer due diligence, monitoring transactions, and reporting suspicious activities. The introduction of this new regulation is significant in the Indonesian agenda of preventing financial institutions from being used for illegal activities, and helps protect the integrity of the financial services sector by ensuring that financial institutions are not used to finance terrorism or the development or acquisition of weapons of mass destruction.

This regulation also shows Indonesia's commitment to support regulations in line with international principles governing anti-money laundering programs and prevention of financing for terrorism and weapons.

Enhanced digital onboarding is now a requirement, no longer a good-to-have

Specific to digital onboarding, or electronic Know Your Customer (eKYC) services, financial organisations need to be aware of the following key changes and ensure processes and tools are in place to meet the compliance requirements:

-

Enhanced Customer Due Diligence (CDD): Stricter regulations demand thorough customer due diligence, including identification and verification of beneficial owners, risk assessments, and ongoing monitoring.

-

Robust Anti-Money Laundering (AML) Measures: organisations must implement comprehensive AML measures to detect and prevent money laundering and terrorism financing activities.

-

Proliferation Financing (PF) Compliance: Financial institutions are required to assess and mitigate the risk of proliferation financing, report suspicious transactions, and strengthen risk mitigation measures.

-

Third-Party Engagement: Revised provisions necessitate proper engagement and verification processes when using third-party services for onboarding, such as eKYC providers.

Best practices and key considerations

To adhere to the latest regulations, FIs will need to consider best practices for their overall AML-CFT and CPF efforts for digital onboarding processes. Some best practices will include:

-

Risk-Based Approach: Implement a risk-based approach to customer due diligence, where you perform necessary KYC and CDD procedures at onboarding process. Following which, a compliance team within the FI should identify, assess, and understand the money laundering and terrorist financing risk to which they are exposed, and take the appropriate mitigation measures in accordance with the level of risk.

-

Advanced Identity Verification: Leverage advanced identity verification solutions that utilise artificial intelligence and machine learning to authenticate identities, detect fraudulent documents, and perform liveness checks.

-

Ongoing Monitoring and Screening: Implement robust transaction monitoring and customer screening mechanisms to identify suspicious activities and ensure ongoing compliance.

-

Strong Data Protection Measures: Employ encryption, data anonymisation, and secure storage to protect customer data. Adhere to data protection regulations, such as GDPR, and establish strict access controls.

FIs should also consider challenges they might encounter when implementing certain changes:

-

As regulation changes, current processes within FIs might require updates or changes in order to comply with updated regulation, and these changes need to be done while maintaining a seamless customer experience for the customers. Organisations will have to strike a balance between compliance, efficiency and overall customer experience.

-

FIs going through digital transformation might not be immediately ready to execute the changes required within their current technologies, and might need to add new solutions to their technology stack, or migrate to a new platform altogether. To enhance current technology stack, FIs must consider deploying or developing robust and agile systems that can quickly adapt to regulatory changes, ensuring compliance while maintaining operational flexibility.

-

For FIs with established workflows for your onboarding, introducing new processes or even new technologies to existing processes can be complex, requiring careful planning and coordination. With the added pressure of a time limit, companies need to ensure thorough planning prior to execution to ensure smoother transition, without unexpected delays.

How can ADVANCE.AI help?

In addition to our compliance expertise to help financial organisations navigate regulatory changes, customize compliance workflows, and ensure adherence to evolving compliance standards, ADVANCE.AI solutions offer comprehensive tools to ensure the transition is smooth, efficient and customer-friendly for your end-users:

-

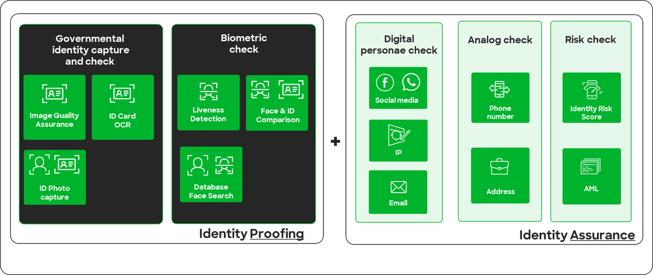

Our eKYC suite of services provides advanced identity verification solutions that employ AI-driven technologies to authenticate identities, perform document verification, and detect fraudulent activities. Our suite of products covers digital identity verification components such as ID Document Verification, Liveness Detection, Face Comparison, biometric technologies, and so much more.

Consider using end-to-end solutions to provide yourself with quicker and easier implementation process

Consider using end-to-end solutions to provide yourself with quicker and easier implementation process

-

Our Anti-Money Laundering solutions, such as watchlist screening, identity risk related scores and data etc, leverage advanced analytics and machine learning to help your organisation to:

-

Build strong and more reliable identity profiles of your customers

-

Screen customer and transaction data against various watchlists, such as government sanctions lists, politically exposed persons (PEP) lists, and other databases, to identify any potential matches or risks

-

-

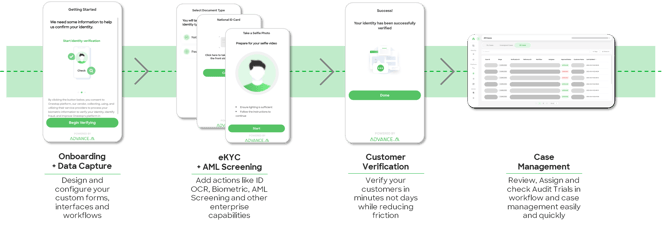

Our OneStop Platform brings together market-leading eKYC and AML capabilities and services onto a single platform to help you:

-

Effortlessly design and orchestrate onboarding workflows and journeys with low to no-code required.

-

Redefine deployment processes by reducing time spent designing, testing and deploying workflows to rapidly meet changing AML, eKYC and Compliance requirements

-

Ensure continuous compliance and auditability by leveraging case management, audit trails, and configurable policies for robust reporting and control.

-

Design your own processes and manage the customer journey - all from a single platform

Design your own processes and manage the customer journey - all from a single platform

Overall, the above will help your organisation better support compliance efforts across of your digital onboarding processes.

Conclusion

As financial organisations navigate the changing landscape of compliance in customer onboarding, embracing digital transformation while ensuring regulatory compliance is crucial. By understanding key changes, overcoming challenges, adopting best practices, and leveraging ADVANCE.AI solutions, organisations can achieve a seamless transition to compliant digital onboarding while delivering an exceptional customer experience.

For more eKYC best practices, head over to our previous blog post on 'A few things you should know about eKYC', or jump right in to a complimentary demo and consultation session with our experts to get started on your eKYC journey.